February Exchange Volumes – Volatility and Volumes Mixed M/M; QTD Volume Trends Show Upside to EPS Estimates

Monthly Recap of Exchange Volumes for February and EPS Impacts for the Exchanges

In February, average volatility metrics generally eased while volumes across the exchange landscape showed mixed results. While February results were mixed, exchange volumes have mainly increased for the quarter both Q/Q and Y/Y, which should lead to increased transaction-based revenues across the exchange landscape. Based on current QTD volume trends, I currently see 1% to 9% upside to exchange EPS estimates for the quarter (assuming volume trends hold steady through quarter end) with ICE showing the strongest QTD volume results (implying 9% EPS upside for the quarter) and NDAQ showing the least amount of upside at 1% (which makes sense given NDAQ’s de-emphasis on transaction based revenue streams).

Source: company documents and my estimates

Industry Wide Volume Recap

Volatility

Average volatility was mixed in February relative to January’s averages as the VIX was up 2% M/M, realized volatility (measured by the daily changes in the S&P 500) was down 21% M/M, volatility of volatility (as measured by the VVIX) was down 2% M/M and treasury volatility (as measured by the MOVE index) was down 4% M/M. Relative to a year ago, average volatility was mixed as well in February with the VIX up 22% Y/Y, realized volatility down 2% Y/Y, the VVIX up 22% Y/Y and the MOVE index down 18% Y/Y.

On a quarter-to-date basis, volatility is mainly lower relative to 4Q24-to-date but generally higher than the year ago quarter-to-date. The average QTD VIX of 16.9 is down 7% Q/Q (+24% Y/Y), while realized volatility is averaging 16.7 (+18% Q/Q, +22% Y/Y), the VVIX is averaging 101.5 (-3% Q/Q, +23% Y/Y) and the MOVE index is averaging 92.9 (-15% Q/Q, -16% Y/Y).

Please note that throughout the entirety of this piece QTD averages are being calculated as through the first two months of the quarter for the current quarter to date, the prior quarter to date and the year ago quarter to date.

Average volatility levels can generally be indicative of trading activity with volumes generally increasing in periods of heightened volatility and decreasing as volatility subsides.

13 Month Trailing Volatility Metrics

Source: Yahoo Finance

U.S. Equities

Average U.S. cash equities volumes (ADV) were up slightly M/M in February at 15.6 billion shares traded per day but increased 33% Y/Y. The Y/Y increase was primarily driven by off-exchange volumes (Trade Reporting Facility or TRF Volume) as TRF volumes were up 54% Y/Y (unchanged M/M) to 7.9 billion traded per day while on-exchange volumes were up 17% Y/Y (+3% M/M) to 7.7 billion traded per day. This marks the 4th consecutive month where TRF activity exceeded that of on-exchange trading volumes.

On a quarter-to-date basis, U.S. equity ADV is higher both sequentially and year over year as volumes are averaging 15.5 billion shares traded per day (+19% Q/Q, +33% Y/Y). QTD growth is being driven by off-exchange volumes with QTD TRF ADV of 7.9 billion (+23% Q/Q, +55% Y/Y) while on-exchange volumes are averaging 7.6 billion shares per day (+16% Q/Q, +16% Y/Y).

13 Month Trailing Average Daily U.S. Cash Equities Volumes

Source: Cboe Global Markets

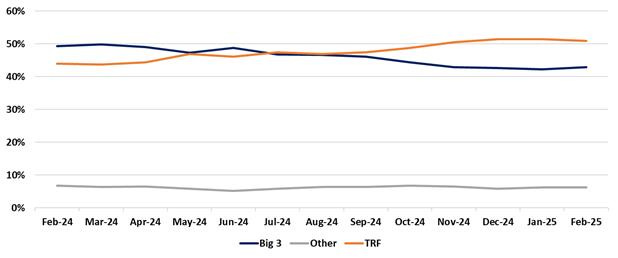

In terms of market share of U.S. cash equities volumes, the big three publicly traded U.S. exchange groups (CBOE, ICE, NDAQ) showed increased market share in February relative to January levels but all three showed substantial Y/Y declines in market share in February. CBOE posted market share of 10.7% in February (+11 bps M/M, -230 bps Y/Y), ICE posted market share of 17.8% in February (+34 bps M/M, -204 bps Y/Y) and NDAQ posted market share of 14.4% (+20 bps M/M, -204 bps Y/Y).

For the quarter-to-date, CBOE market share is averaging 10.7%, (-35 bps Q/Q, -251 bps Y/Y), ICE is averaging 17.7% (-63 bps Q/Q, -231 bps Y/Y) and NDAQ is averaging 14.2% (-9 bps Q/Q, -187 bps Y/Y).

13 Month Trailing U.S. Cash Equities Market Share

Source: Cboe Global Markets

13 Month Trailing U.S. Cash Equities Market Share

Source: Cboe Global Markets

As we can see in the graph below, off-exchange volumes surpassed that of the combined market share of the big 3 publicly traded exchanges in July of 2024 and have continued to remain elevated since. This phenomenon explains why there have been a number of references to the level of off-exchange trading in recent weeks and the potential implications for market structure and market quality in the U.S. and which I referenced in my weekly write-up a few weeks ago (Links: Bloomberg Article on Off-Exchange Trading, Nasdaq 4Q24 earnings presentation showing market share excluding off-exchange volumes, Nasdaq blog post on off-exchange trading increasing across all types of stocks).

13 Month Trailing U.S. Cash Equities Market Share

Source: Cboe Global Markets

U.S. Options, Index Options and OCC Futures Volumes

Average U.S. equity options volumes were up 3% M/M in February at 54.6 million contracts traded per day but increased 23% Y/Y. Meanwhile Index option volumes were down 1% M/M in February to 4.5 million contracts per day (+10% Y/Y) and OCC Futures volumes increased 10% M/M in February to 241k contracts per day (+13% Y/Y).

On a quarter-to-date basis, U.S. equity options ADV is higher both sequentially and year over year as volumes are averaging 53.8 million contracts traded per day (+14% Q/Q, +24% Y/Y). Index options volumes are averaging 4.6 million contracts per day (+11% Q/Q, +10% Y/Y) while OCC Futures volumes are averaging 230k per day (+13% Q/Q, +4% Y/Y).

13 Month Trailing Average Daily U.S. Equity Options, Index and OCC Futures Volumes

Source: OCC

In terms of market share of U.S. equity options volumes, the big three publicly traded U.S. exchange groups (CBOE, ICE, NDAQ) showed mixed results in February relative to January and year ago levels. CBOE posted market share of 24.8% in February (+10 bps M/M, -16 bps Y/Y), ICE posted market share of 18.7% in February (-90 bps M/M, -255 bps Y/Y) and NDAQ posted market share of 29.6% (+15 bps M/M, +8 bps Y/Y).

For the quarter-to-date, CBOE market share is averaging 24.8%, (+40 bps Q/Q, -14 bps Y/Y), ICE is averaging 19.2% (+12 bps Q/Q, -196 bps Y/Y) and NDAQ is averaging 29.0% (-163 bps Q/Q, -51 bps Y/Y).

13 Month Trailing U.S. Equity Options Market Share

Source: OCC

13 Month Trailing U.S. Equity Options Market Share

Source: OCC

Company Specific Updates

Cboe Global Markets, Inc. (CBOE)

CBOE 0.00%↑ volumes ended February mixed as index options and FX volumes declined vs. January levels while equity options, futures and U.S. cash equities increased M/M. U.S. cash equities ADV at CBOE was 1.7 billion for the month, up 2% M/M (+10% Y/Y), and futures volumes at CBOE averaged 241k per day (+10% M/M, +13% Y/Y). Equity options ADV came in at 13.6 million in February (+3% M/M, +22% Y/Y), Index options volumes ended February at 4.5 million per day (-2% M/M, +9% Y/Y) and Global FX volumes ended the month at $48.0 billion per day (-5% M/M, +10% Y/Y).

For the quarter-to-date, volumes across the board are trending up sequentially and are generally up year over year. U.S. equity options ADV is tracking at 13.3 million (+16% Q/Q, +23% Y/Y), Index options ADV is tracking at 4.5 million (+11% Q/Q, +10% Y/Y), futures volumes are tracking at 230k (+6% Q/Q, +4% Y/Y), U.S. equities ADV is tracking at 1.7 billion and Global FX ADNV is tracking at $47.7 billion (+8% Q/Q, +8% Y/Y).

CBOE Key Product Lines Trailing 13 Month ADV

Source: Cboe Global Markets and OCC

In terms of the revenue and EPS impact from the above volume statistics for CBOE, relative to last quarter’s results I see about $17 million in revenue upside to CBOE’s transaction based revenues for 1Q25. This translates into about $0.11 in EPS, or 5% upside relative to what CBOE reported last quarter.

Source: company documents and my estimates

CME Group Inc. (CME)

CME 0.00%↑ total volumes ended February up M/M and Y/Y, though there was some variability amongst major product categories. Total CME ADV increased 29% M/M to 33.1 million contracts per day (+12% Y/Y). Interest rates ADV seasonally increased to 19.2 million per day (+64% M/M, +11% Y/Y), metals ADV increased to 0.8 million (+13% M/M, +34% Y/Y), Ags ADV increased to 2.1 million (+4% M/M, +15% Y/Y), FX ADV increased to 1.1 million (+4% M/M, +25% Y/Y), metals ADV declined to 2.8 million (-13% M/M, +11% Y/Y) and equities ADV increased to 7.2 million (+3% M/M, +9% Y/Y). Note that interest rates ADV typically increases dramatically in the second month of the quarter as quarterly rate contracts expire and roll over activity occurs.

Quarter-to-date total CME volumes are averaging 29.2 million per day (+8% Q/Q, +7% Y/Y). By contract type, Energy ADV has increased to 3.0 million per day (+16% Q/Q, +21% Y/Y), FX ADV has increased to 1.0 million per day (+17% Q/Q, +20% Y/Y), equities ADV has increased to 7.1 million per day (+16% Q/Q, +8% Y/Y), Ags ADV has increased to 2.0 million per day (+8% Q/Q, +24% Y/Y), metals ADV is roughly flat Q/Q at 0.7 million per day (+20% Y/Y) and interest rates ADV has increased to 15.2 million per day (+3% Q/Q, +1% Y/Y).

CME Key Product Lines Trailing 13 Month ADV

Source: CME Group Inc.

In terms of the revenue and EPS impact from the above volume statistics for CME, relative to last quarter’s results I see about $88 million in revenue upside to CME’s transaction based revenues for 1Q25. This translates into about $0.19 in EPS, or 7% upside relative to what CME reported last quarter.

Source: company documents and my estimates

Intercontinental Exchange, Inc. (ICE)

ICE 0.00%↑ volumes generally declined M/M in February but were mainly higher Y/Y. Total futures ADV declined to 9.7 million (-1% M/M, +17% Y/Y) as energy ADV declined to 5.5 million (-2% M/M, +25% Y/Y), interest rate ADV declined to 3.3 million (-4% M/M, +17% Y/Y) and other financials ADV increased to 0.3 million (+1% M/M, -1% Y/Y) while ags & metals ADV increased to 0.6 million per day (+24% M/M, -16% Y/Y). U.S. options volumes declined to 10.2 million per day (-2% M/M, +8% Y/Y) while U.S. equities volumes increased to 2.8 billion per day (+1% M/M, +18% Y/Y).

For the quarter-to-date, ICE’s volumes are generally tracking higher both Q/Q and Y/Y with total futures ADV increasing to 9.8 million per day (+8% Q/Q, +19% Y/Y), U.S. options increasing to 1032 million per day (+15% Q/Q, +13% Y/Y) and U.S. equities ADV increasing to 2.7 billion per day (+15% Q/Q, +16% Y/Y).

ICE Key Product Lines Trailing 13 Month ADV

Source: Intercontinental Exchange, Inc., Cboe Global Markets and OCC

In terms of the revenue and EPS impact from the above volume statistics for ICE, relative to last quarter’s results I see about $104 million in revenue upside to ICE’s transaction based revenues for 1Q25. This translates into about $0.14 in EPS, or 9% upside relative to what ICE reported last quarter.

Source: company documents and my estimates

Nasdaq, Inc. (NDAQ)

NDAQ 0.00%↑ volumes increased both M/M and Y/Y in February. U.S. equities ADV increased to 2.2 billion (+3% M/M, +17% Y/Y) while U.S. equity options ADV increased to 16.1 million (+7% M/M, +23% Y/Y).

Quarter-to-date, NDAQ volumes have increased by sequentially and Y/Y. U.S. equities ADV is tracking at 2.2 billion (+18% Q/Q, +18% Y/Y) and U.S. options ADV has increased to 15.6 million (+8% Q/Q, +22% Y/Y).

NDAQ Key Product Lines Trailing 13 Month ADV

Source: Cboe Global Markets and OCC

In terms of the revenue and EPS impact from the above volume statistics for NDAQ, relative to last quarter’s results I see about $7 million in revenue upside to NDAQ’s transaction based revenues for 1Q25. This translates into about $0.01 in EPS, or 1% upside relative to what NDAQ reported last quarter.