Weekly Recap for Week Ended August 8, 2025

Weekly Recap of Major Micro / Macro Data Points and Things to Look Forward to in the Week Ahead

Company Specific Updates for Week Ended Aug. 8, 2025

Exchanges

Cboe Global Markets, Inc. (CBOE)

Surpasses 1,000 U.S. listed ETFs

CBOE has welcomed 185 new ETFs YTD

CBOE currently second largest ETF listing venue in U.S.

Reports July Volumes

Total option volumes were up 1% M/M, up 10% Y/Y

Futures volumes were down 4% M/M, down 33% Y/Y

U.S. equities volumes were up 1% M/M, up 40% Y/Y

Canada equities volumes were up 3% M/M, up 22% Y/Y

E.U. equities volumes were up 6% M/M, up 35% Y/Y

Australian equities volumes were down9% M/M, up 13% Y/Y

Japan equities volumes were down 75% M/M, down 86% Y/Y

Clearing volumes were up double digits M/M and Y/Y

FX volumes were down 5% M/M, up 6% Y/Y

CBOE July Monthly Volumes

Source: company documents

CME Group Inc. (CME)

Farmer sentiment continues to weaken but farmers believe U.S. policy headed in right direction

Farmer sentiment barometer fell 11 points from June to 135

Declares quarterly dividend of $1.25 (unch)

Reports July Volumes

As mentioned in my exchange volume piece out Friday (link below), $CME July Volume declined 15% M/M (-12% Y/Y)

RPCs for June were released with earnings so nothing new there

BrokerTec volumes were down M/M in July but mixed Y/Y

EBS volumes were down 12% M/M (-9% Y/Y)

See table for official July volume statistics

CME July Volume (M) and June RPCs

Source: company documents

Intercontinental Exchange, Inc. (ICE)

Appoints President of NYSE Texas

Bryan Daniel appointed as President of the exchange, reporting to Lynn Martin, President of NYSE Group

Mr. Daniel has extensive public policy experience, most recently serving as the Chairman of the Texas Workforce Commission. Also previously served on Governor Greg Abbott’s senior staff where he led the Office of Economic Development and Tourism

Additionally, NYSE signed a lease to establish the headquarters of NYSE Texas in the Old Parkland campus in Dallas. New location expected to open in 2026

Mizuho Americas Joins ICE Clear Credit as Clearing Member

Reports July Volume

As mentioned in my post last Friday futures ADV -21% M/M (+12% Y/Y). Equity options ADV +7% M/M (+6% Y/Y). U.S. equity ADV -5% M/M (+56% Y/Y)

Futures RPC for July +1% M/M (+2% Y/Y)

Equity options RPC -17% M/M (unch Y/Y)

Equity RPC -3% M/M (-35% Y/Y)

ICE July Volume and RPCs

Source: company documents

Nasdaq, Inc. (NDAQ)

Reports July Volume

As mentioned in my exchange volume piece out last week, U.S. Equity ADV was down 2% M/M (+35% Y/Y) and U.S. Option ADV was down 3% M/M (+7% Y/Y)

E.U Derivatives ADV down 25% M/M (unch. Y/Y)

E.U. Equities ADV down 7% M/M (+14% Y/Y)

Ests. should not change on this

NDAQ July Official ADV

Source: company documents

Fixed Income Trading Platforms

MarketAxess Holdings Inc. (MKTX)

Announces launch of Mid-X in US Credit

Mid-X is an anonymous mid-point matching session

Was launched in 2024 for EM and Eurobonds

2Q25 EM and Eurobond volumes increased 70% Y/Y on Mid-X protocol

Reports 2Q25 earnings

Beats EPS on adjusted basis but misses on GAAP

Full recap available here

Files 2Q25 10Q

Reports July Trading Volumes

Total credit ADV was $14.3B (-8% M/M, +12% Y/Y)

Total rates ADV was $22.6B (-18% M/M, +1% Y/Y)

Market share for USHG was 17.7% (down 205bps M/M, down 89bps Y/Y)

Market share for USHY was 11.5% (down 84bps M/M, down 101bps Y/Y)

Full recap of fixed income volumes in July available here

MKTX Reported Monthly ADV and Market Share Statistics

Source: company documents

Tradeweb Markets Inc. (TW)

Reports July Trading Volumes

Rates ADV $1.3T (-5% M/M, +13% Y/Y)

Credit ADV $28B (-4% M/M, +6% Y/Y)

Equities ADV $21B (-11% M/M, -7% Y/Y)

Money Markets ADV $1.0T (+1% M/M, +63% Y/Y)

USHG market share 19.6% (+2bps M/M, +171bps Y/Y)

USHY market share 7.9% (-15bps M/M, -111bps Y/Y)

Full recap of fixed income volumes in July available here

TW Reported Monthly ADV and Market Share Statistics

Source: company documents

Online Brokers

eToro Group Ltd. (ETOR)

Leverages AI to Redefine Social Investing

Launching a suite of AI tools expected to transform social investing

Allow users to develop bespoke trading algorithms and automate strategies

Automate trade execution

Integrate real-time market data and third-party tools

Personalize portfolio optimization

Create personalized dashboards for monitoring portfolios

Launching eToro’s AI companion, Tori

eToro has already launched seven Alpha Portfolios as part of its Smart Portfolio offering

Robinhood Markets, Inc. (HOOD)

Schedules date for July Metrics release

Wednesday, August 13 at 4:05pm ET

Announces HOOD summit 2025

September 9-10 in Las Vegas

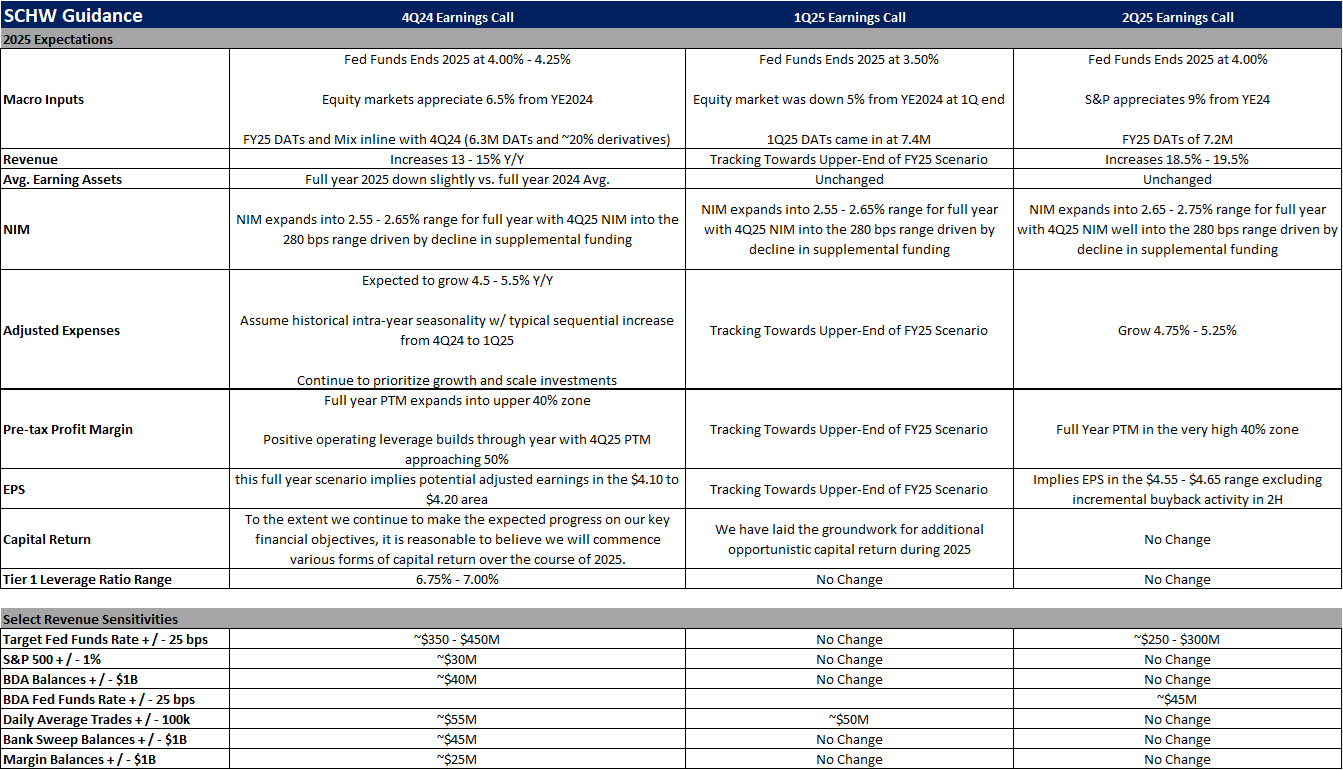

The Charles Schwab Corporation (SCHW)

Cautious Optimism in July as STAX Score Edges Upward

STAX increased to 41.79 from 40.66 in June

SCHW clients were net sellers in July

Net selling highest in Information Technology sector

Net buying highest in Communication Services, Health Care and Fins

Company Specific Updates Anticipated for the Upcoming Week (Ended Aug. 15, 2025)

Exchanges

None to Note

Fixed Income Trading Platforms

None to Note

Online Brokers

eToro Group Ltd. (ETOR)

2Q25 Earnings Release Tuesday, August 12 (pre-market)

Conference call 8:30am ET

Robinhood Markets, Inc. (HOOD)

July Monthly Metrics

Wednesday, August 13 (post-close)

The Charles Schwab Corporation (SCHW)

July Monthly Metrics

Thursday, August 14 (pre-market)

Next Four Weeks Calendar

Source: Company press releases and my estimates around timing

Major Macro Updates for Week Ended Aug. 8, 2025

Factory Orders (Jun.) – (4.8%) vs. consensus (4.9%) and prior 8.3%

U.S. Trade Deficit (Jun.) – ($60.2B) consensus ($61.0B) and prior ($71.7B)

S&P Final U.S. Services PMI (Jul.) – 55.7 vs. prior 52.9

ISM Services (Jul.) – 50.1% vs. consensus 51.1% and prior 50.8%

Initial Jobless Claims (week ended Aug. 2) – 226k vs. consensus 221k and prior 219k

U.S. Productivity (2Q) – 2.4% vs. consensus 1.9% and prior (1.8%)

U.S. Unit Labor Costs (2Q) – 1.6% vs. consensus 1.3% and prior 6.9%

Wholesale Inventories (Jun.) – 0.1% vs. prior (0.3%)

Major Macro Updates Scheduled for the Upcoming Week (Ended Aug. 15, 2025)

Monday, Aug. 11

None to Note

Tuesday, Aug. 12

NFIB Optimism Index (Jul.) – consensus 99.0 and prior 98.6

Consumer Price Index (Jul.) – consensus 0.2% and prior 0.3%

CPI Y/Y (Jul.) – consensus 2.8% and prior 2.7%

Core CPI (Jul.) – consensus 0.3% and prior 0.2%

Core CPI Y/Y (Jul.) – consensus 3.1% and prior 2.9%

Monthly Federal Budget (Jul.) – consensus $227.7B and prior 244B

Wednesday, Aug. 13

None to Note

Thursday, Aug. 14

Initial Jobless Claims (week ended Aug. 9) – consensus 229k and prior 226k

Producer Price Index (Jul.) – consensus 0.2% and prior 0.0%

Core PPI (Jul.) – consensus 0.3% and prior 0.0%

PPI Y/Y (Jul.) – prior 2.3%

Core PPI Y/Y – prior 2.5%

Friday, Aug. 15

Retail Sales (Jul.) – consensus 0.5% and prior 0.6%

Retail Sales Minus Autos (Jul.) – consensus 0.3% and prior 0.5%

Empire State Manufacturing Survey (Aug.) - consensus 1.8 and prior 5.5

Import Price Index (Jul.) – consensus 0.0% and prior 0.1%

Import Price Index Minus Fuel (Jul.) – prior 0.1%

Industrial Production (Jul.) – consensus 0.0% and prior 0.3%

Capacity Utilization (Jul.) – consensus 77.6% and prior 77.6%

Business Inventories (Jun.) – consensus 0.2% and prior 0.0%

Preliminary Consumer Sentiment (Aug.) – consensus 62.5% and prior 61.7%

Exchange Volume Update

Exchange Volumes Over Past Week and W/W Trends

For the week ended August 8, 2025, volumes were lower as volatility was mixed W/W.

The average VIX for the week was flat with the prior week, average realized volatility was up 36% W/W, average volatility of volatility (as measured by the VVIX) was down 1% W/W and the average MOVE index (U.S. Treasuries volatility) was up 2% W/W.

Futures average daily volumes (ADV) were lower as CBOE futures volumes were down 15% W/W, CME futures volumes were down 21% W/W, and ICE futures volumes were down 14% W/W.

Total U.S. Equities ADV was down 12% W/W, as TRF volumes fell 13% W/W while on-exchange volumes were down 12% W/W. Industry equity options volumes were down 3% W/W while index options volumes fell 14% W/W.

For further detail on weekly volume trends by exchange and by product line please see the charts below.

CME Futures Volumes (M)

Source: Company Daily Volume Releases

ICE Futures (M), U.S. Equities (B) and U.S. Equity Options (M) Volumes

Source: Company Daily Volume Releases, Cboe Global Markets and OCC

CBOE Options (M), Futures (K), U.S. Equity (B), and FX Volumes ($B)

Source: Company Daily Volume Releases and OCC

NDAQ U.S. Equity (B) and Option (M) Volumes

Source: Cboe Global Markets and OCC

U.S. Total Industry Equity Volumes (B)

Source: Cboe Global Markets

U.S. Total Industry Equity Option and Index Option Volumes (M)

Source: OCC

Volatility Metrics

Source: Yahoo Finance

Exchange Volumes MTD / QTD / YTD Trends

For the month to date, exchange volumes are trending mixed vs. July and mixed Y/Y. This comes as volatility is mainly higher M/M but lower on a Y/Y basis.

The average VIX in August is down 10% Y/Y while realized volatility is down 54% Y/Y and volatility of volatility is down 14 Y/Y. Treasuries volatility is also lower Y/Y as the average MOVE index in August is down 24% Y/Y.

Futures volumes are lower Y/Y as ICE futures ADV is down <1% vs. August 2024 ADV. Meanwhile, CME ADV is down 16% Y/Y while CBOE futures ADV is down 22% Y/Y.

In terms of equities and options volumes, total U.S. equities ADV is up 50% MTD while option volumes are up 30% for equity options and up 14% for index options.

For further details on MTD, QTD and YTD ADV please see the charts below.

CME Futures Volumes (M)

Source: Company Daily Volume Releases

ICE Futures (M), U.S. Equities (B) and U.S. Equity Options (M) Volumes

Source: Company Daily Volume Releases, Cboe Global Markets and OCC

CBOE Options (M), Futures (K), U.S. Equity (B), and FX Volumes ($B)

Source: Company Daily Volume Releases and OCC

NDAQ U.S. Equity (B) and Option (M) Volumes

Source: Cboe Global Markets and OCC

U.S. Total Industry Equity Volumes (B)

Source: Cboe Global Markets

U.S. Total Industry Equity Option and Index Option Volumes (M)

Source: OCC

Volatility Metrics

Source: Yahoo Finance

Major Indices, Interest Rates and Company Share Price Trends

The market closed out the week higher, rising 240bps W/W. Yields were higher while the curve flattened a bit and the VIX was down 26% on the week.

In terms of the companies I follow, BULL and HOOD showed the strongest performance, rising 13% and 15%, respectively, W/W. Rounding out eBroker land, ETOR was unchanged on the week, IBKR rose 4% and SCHW was up 2%. Within fixed income trading land, TW fell 1% while MKTX was down 10% after reporting an underwhelming 2Q and disappointing July market share figures. Within the exchanges, all exchange companies rose 1-2%.

Source: Yahoo Finance, FRED, U.S. Department of the Treasury

Comp Sheet

Source: Yahoo Finance

Guidance Tracker

Exchanges

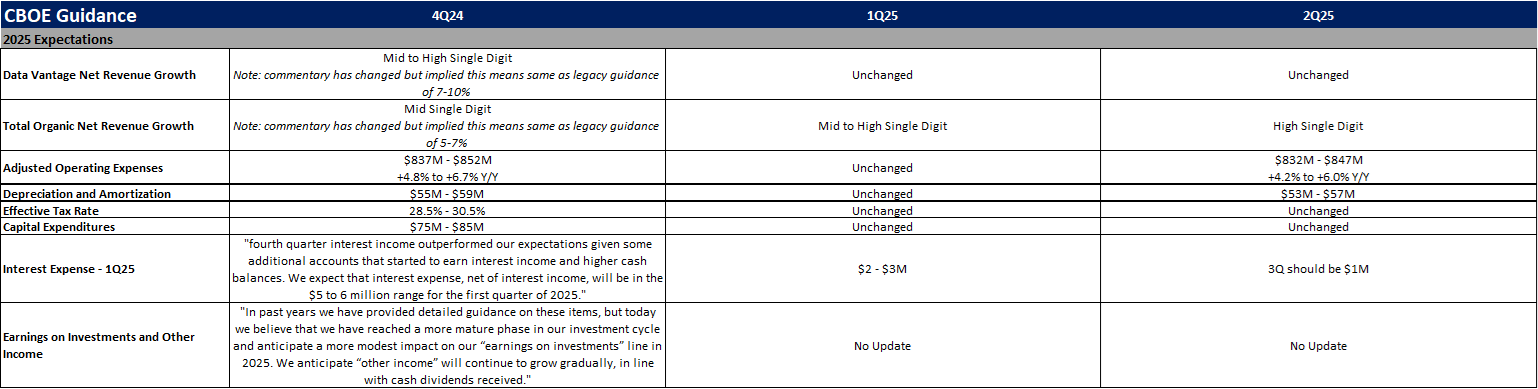

Cboe Global Markets, Inc. (CBOE)

Source: Company documents

Note: CBOE provided additional guidance points / commentary on its 2Q25 earnings call, but key annual highlights are included above for the sake of simplicity

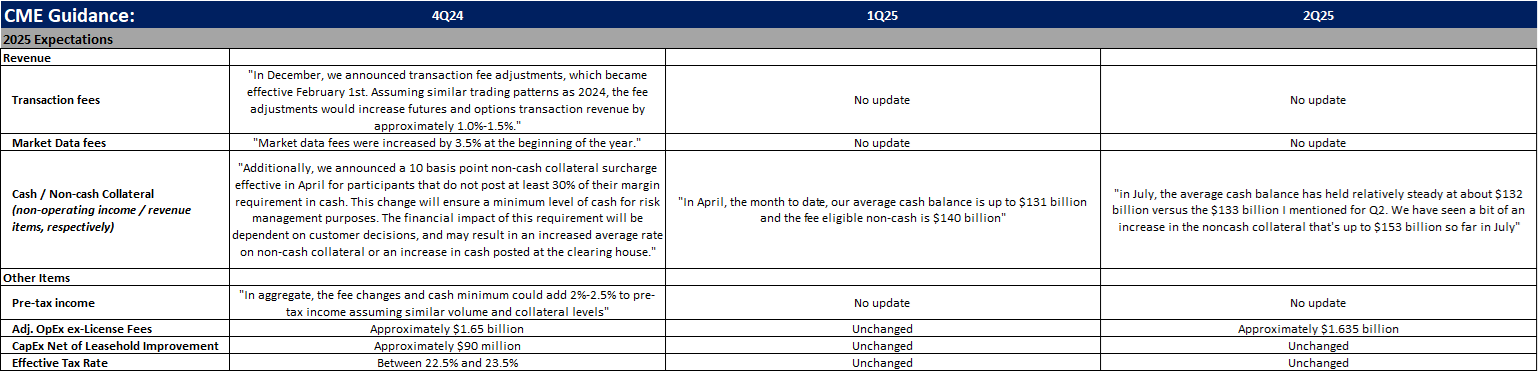

CME Group Inc. (CME)

Source: Company documents

Note: CME provided additional guidance points / commentary on its 2Q25 earnings call, but key annual highlights are included above for the sake of simplicity

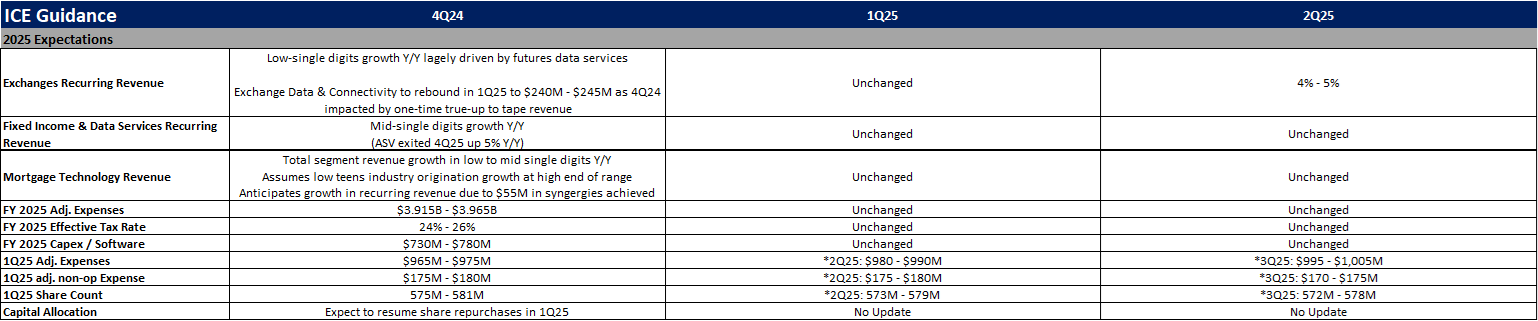

Intercontinental Exchange, Inc. (ICE)

Source: Company documents

Note: ICE provided additional guidance points / commentary on its 2Q25 earnings call, but key annual highlights are included above for the sake of simplicity

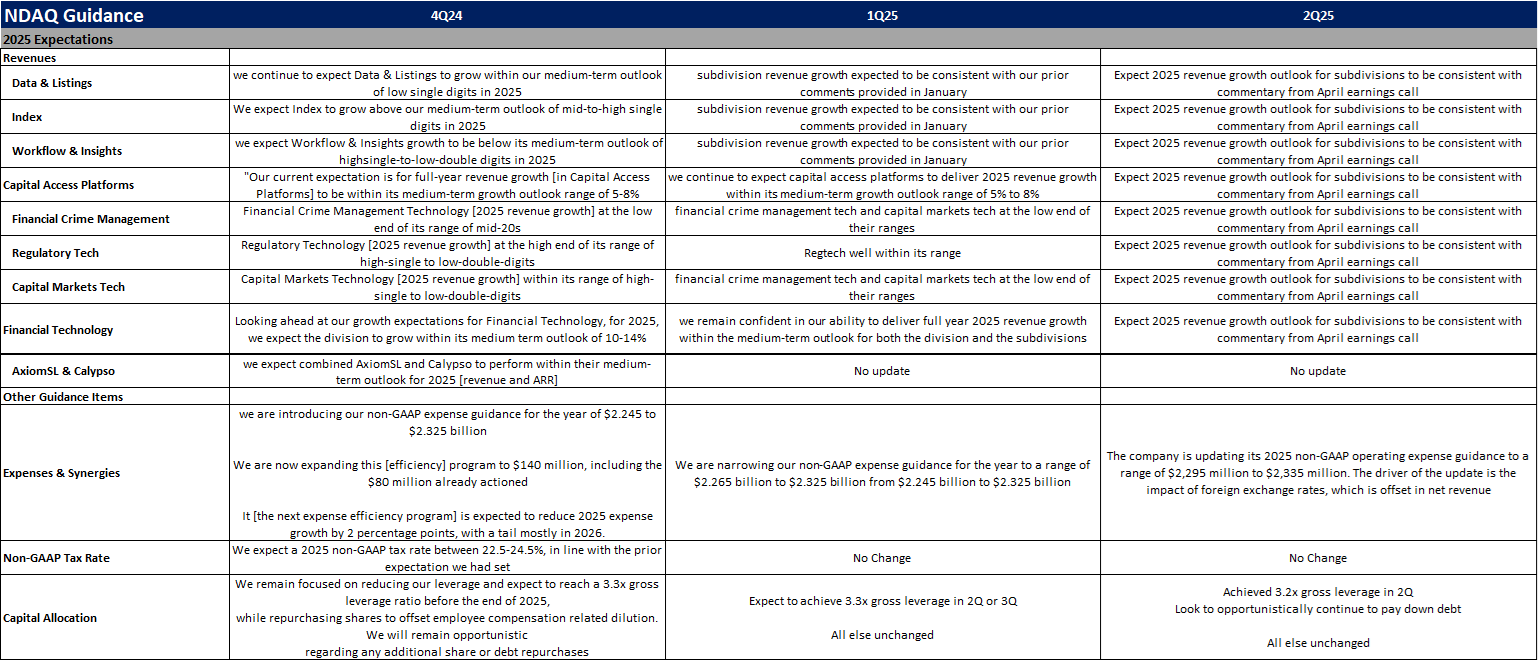

Nasdaq, Inc. (NDAQ)

Source: Company documents

Note: NDAQ provided additional guidance points / commentary on its 2Q25 earnings call, but key annual highlights are included above for the sake of simplicity

Fixed Income Trading Platforms

MarketAxess Holdings Inc. (MKTX)

Source: Company documents

Note: MKTX provided additional guidance points / commentary on its 2Q25 earnings call, but key annual highlights are included above for the sake of simplicity

Tradeweb Markets Inc. (TW)

Source: Company documents

Note: TW provided additional guidance points / commentary on its 2Q25 earnings call, but key annual highlights are included above for the sake of simplicity

Online Brokers

Robinhood Markets, Inc. (HOOD)

Source: Company documents

Note: HOOD provided additional guidance points / commentary on its 2Q25 earnings call, but key annual highlights are included above for the sake of simplicity

Interactive Brokers Group, Inc. (IBKR)

Source: Company documents

Note: IBKR provided additional guidance points / commentary on its 2Q25 earnings call, but key annual highlights are included above for the sake of simplicity

The Charles Schwab Corporation (SCHW)