Robinhood Markets, Inc. (HOOD) 1Q25 Earnings Review

Earnings Beat Consensus Estimates as Transaction Revenue Continues to be Strong; April Activity Indicates 2Q Off to a Solid Start

EPS Beats Consensus Forecast as Revenue Comes in 1% Above Expectations

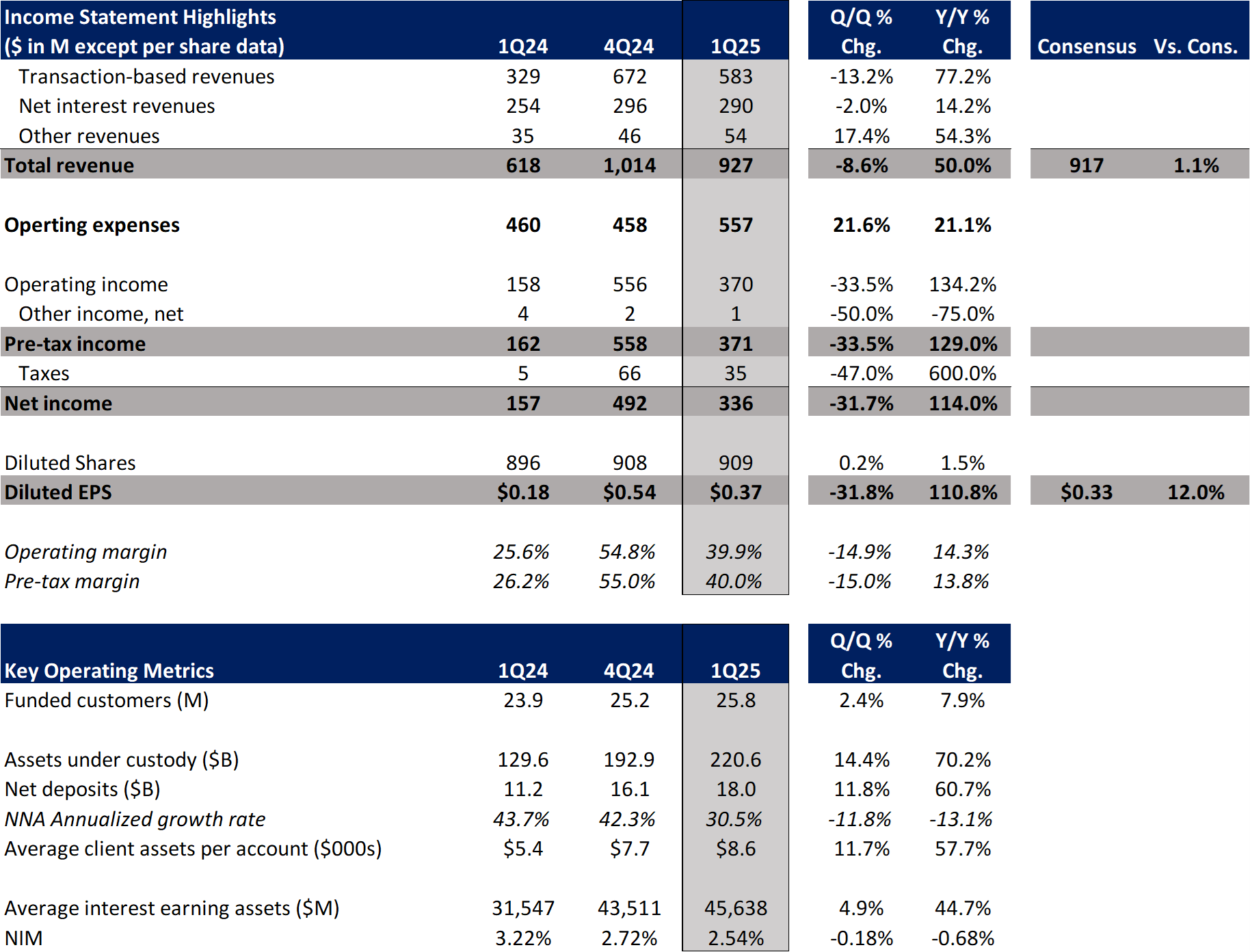

HOOD reported 1Q25 earnings post-market close this evening. Total revenue came in at $927M, down 9% Q/Q but up 50% Y/Y. The sequential decline in revenue was driven by a decrease in transaction-based revenues, which fell 13% Q/Q but were up 77% Y/Y to $583M. Meanwhile, net interest revenue increased 2% Q/Q (+14% Y/Y) to $290M and other revenue increased 17% Q/Q (+54% Y/Y) to $54M. On the expense side, operating expenses came in at $557M, up 22% sequentially (+21% Y/Y) and drove operating margins to 39.9% (down 14.9 percentage points Q/Q but up 14.3 percentage points Y/Y). Non-operating income came in at $1M (-50% Q/Q, -75% Y/Y) and diluted EPS came in at $0.37, down 32% Q/Q (+110% Y/Y).

Relative to consensus estimates, revenue came in 1% above the consensus forecast of $917M. Meanwhile, EPS came in 12% above consensus.

In terms of key operating metrics, total funded customers came in at 25.8M (+2% Q/Q, +8% Y/Y), assets under custody (now referred to as Total Platform Assets following the acquisition of TradePMR at the end of February) ended the quarter at $220.6B (+14% Q/Q, +70% Y/Y), and net deposits for the quarter amounted to $18.0B (+12% Q/Q, +61% Y/Y), implying an annualized growth rate of 30.5% (note, my calculated annualized growth rate adjusts the denominator for the $42.9B of acquired assets from the TradePMR acquisition in February). Average interest earning assets for the quarter came in at $45.6B and the net interest margin (NIM) came in at 2.54% (-18bps Q/Q).

HOOD Earnings Summary and Key Operating Metrics

Source: company data and Tikr.com

Highlights from HOOD Earnings Call, Presentation and Press Release

In terms of the outlook going forward, HOOD 0.00%↑ management touched on several details during this evening’s earnings call that are worth highlighting:

Expenses – Adjusted operating expense guidance increased to $2.085B - $2.185B due to the inclusion of TradePMR. Updated guidance does not include provision for credit losses (amounted to $24M in 1Q25) or the pending acquisition of Bitstamp. The $85M of increased cost for TradePMR does include deal-related costs, which HOOD expects to come out of the run-rate fairly quickly

April Activity Levels – Net deposits are about $6.5B (implies an annualized growth rate of about 36%). Equities trading is at a 4-year high, options trading is near an all-time record, and crypto trading is above $8B. Margin balances are at $8.4B (which would imply a decline of about 5% from the end of March – recall that two weeks ago IBKR had noted its April margin balances had declined about 12% from the end of March)

Interest Rate Sensitivity – Based on current balances, the company believes a 25-basis point cut to the Fed Funds rate would be about a $50 million headwind to NII

Capital Return – Board approved an increase in the buyback authorization of $500M. Since the initial buyback program was announced in May 2024 through April 25, 2025, HOOD has used $667M to repurchase 20M shares. Remaining authorization outstanding currently stands at $833M. Share repurchases in 1Q amounted to 7.2M shares ($322M), which more than offset the shares issued in connection with the TradePMR acquisition

Other notable highlights from the earnings call/press release:

Customer Acquisition – In March, HOOD ran a 2% match promotion on customers transferring into HOOD. Management noted that it helped bring in the record number of deposits in the month and that the customers transferring in tended to be larger customers with an average of $90k transfer per user with taxable accounts even higher at $180k per transfer. Management also noted that the promotions have been very attractive economically for the company with low payback periods

Crypto Pricing – In April, take rates on crypto have been similar to the 1Q levels. HOOD mentioned that they are experimenting with volume-based pricing tiers for crypto, which could drive further volume to the platform in the future

Prediction Markets Business – Have traded over 1B contracts in the past 6 months. Less than half of the 1B traded has been sports related. HOOD continues to be excited about this product and plans to continue to add a wide variety of contracts over time

Futures Trading – After launching futures trading in 1Q, April futures volumes have passed 4.5M, which is larger than all of 1Q. Robinhood mentioned that they believe that futures trading is incremental to the volumes they are getting from current customers as the addition of futures has opened up new behaviors of trading either through the ability to take short positions or trade around the clock which has benefited its active trader segment

Broad Thoughts / Outlook

I thought this was a good quarter out of HOOD. Revenue growth remained really strong Y/Y (though continued to be bolstered by heightened levels of crypto trading). While expenses were slightly elevated relative to the implied quarterly run rate based on HOOD guidance, this was likely driven by higher trading related costs given strong transaction-based revenues and mgmt. reiterated its expense guide for the full year (after accounting for TradePMR). Further, operating margins were solid even with the slightly elevated expenses. The company continues to bring in new customers at a solid clip and asset gathering continues to impress. I would not be surprised to see the stock react positively tomorrow to these results.